Relatives Who Do Not Live With You in Publication 501: Navigating Dependent Claims

Publication 501 (2024) is a crucial resource for understanding the intricate rules surrounding dependents for tax purposes. This guide, while comprehensive, can be overwhelming for taxpayers, particularly when dealing with relatives who don't reside with them. This article simplifies the complexities of claiming dependents, especially those not living under the same roof, to help you navigate the process confidently.

- Understanding the Qualifying Child Tests

- Support, Residency, and Joint Returns

- Decoding the Rules for Divorced and Separated Parents

- The Support Test: Beyond Financial Contributions

- Multiple Claimants: Navigating Tiebreakers

- Emancipation, Special Cases, and Filing Status

-

Frequently Asked Questions Regarding Relatives Not Living With You (Publication 501)

- Q: Can I claim a relative who doesn't live with me as a dependent?

- Q: What are the relationship requirements for claiming a non-resident relative?

- Q: My child lives with an ex-spouse for over half the year. Can I still claim them?

- Q: What about different residency scenarios?

- Q: How is financial support determined for non-resident dependents?

- Q: What if multiple people can claim my relative as a dependent?

- Q: What are the age requirements for non-resident dependents?

- Q: What are the implications if my relative is a student?

- Q: My relative is emancipated; can I still claim them?

- Q: What if my relative was born or died during the tax year?

- Q: How do temporary absences affect residency requirements?

- Q: My relative is a foster child; how does that affect my ability to claim them?

- Q: What are the implications for filing status and credits?

- Q: What about divorced or separated parents?

- Q: What is the income threshold for a qualifying relative?

- Q: Do I need to file Form 8332 for all non-resident dependents?

- Q: Where can I find the most up-to-date information?

Understanding the Qualifying Child Tests

The IRS defines qualifying children based on specific criteria. Understanding these criteria is vital, especially if you have relatives who do not live with you. These tests are not always straightforward, so it's essential to review each one carefully.

The foundational concept is that the relationship must be familial, meaning the individual is a child, stepchild, adopted child, foster child, or sibling. Additionally, the child must meet the age requirement. Generally, a child must be under the age of 19 (or under 24 if a full-time student), unless permanently and totally disabled. Naturally, considering the age of the individual is critical to determining eligibility. Furthermore, the child must live with the taxpayer for more than half the year. This is a crucial factor for those with relatives living apart.

Support, Residency, and Joint Returns

Providing more than half of the child's support is another key consideration. This includes financial support, but it's not simply about the amount; it encompasses all contributions to the child's well-being. The taxpayer must document these contributions. Residency isn't always simple, especially when considering multiple homes and varying living arrangements. The child needs to live with the taxpayer for more than half the year. Finally, if the child is claimed on someone else's joint return, this often prevents you from claiming them as a dependent. This consideration becomes crucial in situations involving divorced or separated parents.

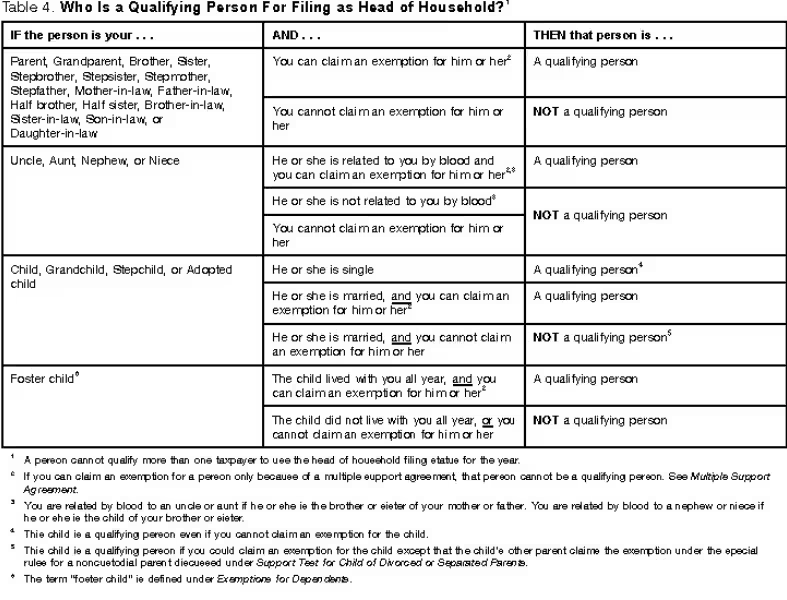

Decoding the Rules for Divorced and Separated Parents

The publication emphasizes special rules for divorced or separated parents. The custodial parent is often the one who can claim the child, but the rules are more elaborate than this. This designation often relates to the parent the child lives with for over half the year, and a written agreement or court decree may override this. If the child spends equal time with both parents, the parent with the lower adjusted gross income (AGI) often claims the child. This is the "tie-breaker rule" and is a crucial point for divorced or separated couples. Understanding the different rules stemming from pre-1985 decrees or agreements is essential for accuracy. A key aspect is the release of claim form (Form 8332), which allows the non-custodial parent to claim the child. It's essential to note that releasing the claim doesn't typically affect the custodial parent's ability to claim the child for other important tax benefits, making careful consideration of the scenario critical.

The Support Test: Beyond Financial Contributions

The support test, while seemingly straightforward, can be surprisingly complex. It's not simply about financial contributions but also about providing over half of the dependent's total care. Things like housing, food, clothing, and medical expenses all count toward the support. The worksheet in Publication 501 is a valuable tool for calculating the extent of your support. It's important to note that governmental aid or scholarships received by the child don't count against the support calculation. In cases of foster care, expenses incurred in caring for the child are often treated as support unless they are deductible as charitable contributions. Naturally, the specifics of the support provided need to be documented.

The publication tackles the tricky situation where a child might meet the qualifying criteria for multiple taxpayers. These situations, such as those involving divorced or separated parents or other family members, require tiebreaker rules to determine who gets to claim the child. The rules often prioritize parents, then joint filers, and then the person with the higher AGI, which impacts who can claim the tax benefits associated with the child. Consider the child tax credit, head of household status, and specific credits, like child and dependent care or earned income credit. Naturally, the IRS dictates which person is officially authorized to claim the child.

Emancipation, Special Cases, and Filing Status

Emancipated children are no longer considered dependents of either parent. The publication also addresses birth and death during the tax year, adoption, foster care, and even kidnapping, providing specific guidelines for these unique situations. Temporary absences, such as those due to hospitalization, are also considered in determining a child's residency. These factors are crucial in calculating the support and residency tests. The publication highlights how the child's dependency status affects different tax benefits, such as the earned income credit and head of household status. A clear understanding of these different tax situations is important when dealing with relatives who don't live with you.

Publication 501 (2024) is a detailed guide for claiming dependents and is quite comprehensive in its analysis. However, understanding the nuanced rules, especially when dealing with relatives who do not live with you, requires careful consideration of the qualifying child and relative tests. Divorced or separated parents, multiple claimants, and special cases all have unique rules. It's crucial for taxpayers to meticulously review the publication and potentially seek professional tax advice to ensure accurate and compliant filings. This meticulous approach is naturally important to avoid potential errors and ensure proper tax filing.

Frequently Asked Questions Regarding Relatives Not Living With You (Publication 501)

This section addresses common questions about claiming relatives who do not live with you as dependents on your tax return, based on IRS Publication 501 guidelines.

Q: Can I claim a relative who doesn't live with me as a dependent?

A: Yes, but there are specific rules for claiming a "qualifying relative." You must meet several criteria, including that the relative's gross income is below a certain threshold, and you provide over half of their support. Crucially, the relative cannot be claimed as a dependent by anyone else. Different rules apply for claiming a "qualifying child," which often involves residency with the taxpayer.

Q: What are the relationship requirements for claiming a non-resident relative?

A: The relationship must meet the criteria of a qualifying relative, which includes specific familial ties. The relationship, while important, is just one of several factors to consider, including income thresholds and support, as outlined in Publication 501.

Q: My child lives with an ex-spouse for over half the year. Can I still claim them?

A: Often, the custodial parent, determined by the parent with whom the child lives for more than half the year, can claim the child. However, if the child spends equal time with both parents, adjusted gross income (AGI) may be a tie-breaker. If you are the non-custodial parent, a release of claim form (Form 8332) might be required to claim the child. This form's use and implications are detailed in Publication 501.

Q: What about different residency scenarios?

A: Publication 501 details rules for various residency situations, including children who live with both parents before separation, or those who spend equal time with each parent. The residency rules are often case-specific, making it imperative to review the detailed guidance in Publication 501.

Q: How is financial support determined for non-resident dependents?

A: For qualifying relatives, you must provide over half of their support. Publication 501 provides a worksheet to assist with this calculation. Governmental aid or scholarships received by the relative are typically not considered part of their support calculation.

Q: What if multiple people can claim my relative as a dependent?

A: Publication 501 outlines tiebreaker rules in these situations, prioritizing parents, joint filers, and then individuals with higher AGI. The IRS determines the rightful claimant for tax benefits.

Q: What are the age requirements for non-resident dependents?

A: Age requirements for qualifying children vary based on whether the child is a student or disabled. Generally, the child must be younger than the taxpayer (or spouse, if filing jointly). There are no age restrictions for qualifying relatives who are permanently and totally disabled.

Q: What are the implications if my relative is a student?

A: Publication 501 specifies age guidelines for students, usually under 24. A qualifying child who is a full-time student may also meet the criteria to be claimed as a dependent.

Q: My relative is emancipated; can I still claim them?

A: An emancipated child is not considered a dependent living with either parent.

Q: What if my relative was born or died during the tax year?

A: Publication 501 outlines specific rules for determining residency and support in cases involving children born or who died during the tax year.

Q: How do temporary absences affect residency requirements?

A: Temporary absences, such as for hospitalization, are usually considered in determining residency requirements. Publication 501 provides clarity for such cases.

Q: My relative is a foster child; how does that affect my ability to claim them?

A: Expenses incurred in caring for a foster child are considered support if not deductible as charitable contributions. Publication 501 details these specific situations.

Q: What are the implications for filing status and credits?

A: The dependent's status affects various tax benefits, especially the earned income credit and head of household status. Publication 501 provides a detailed clarification of how this impacts tax filing.

Q: What about divorced or separated parents?

A: Publication 501 details intricate rules for determining the custodial parent and claiming children in these complex family situations.

Q: What is the income threshold for a qualifying relative?

A: The relative's gross income must fall below a specified threshold to qualify. This threshold can change from year to year and is detailed in IRS Publication 501.

Q: Do I need to file Form 8332 for all non-resident dependents?

A: Form 8332 is often required for non-custodial parents to claim a child, especially in post-2008 divorce decrees or agreements. However, the specific rules and requirements are outlined in Publication 501 and should be consulted for clarification.

Q: Where can I find the most up-to-date information?

A: Always refer to the most current version of IRS Publication 501 for the most accurate and up-to-date information. Tax laws are subject to change.

These FAQs provide general guidance. Individual situations may vary, and consulting a qualified tax professional is highly recommended.