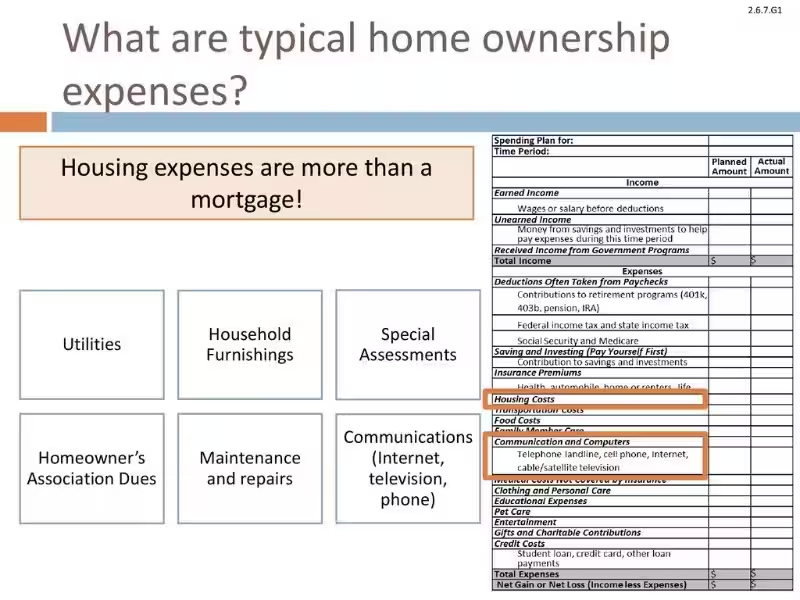

A Major Expense Associated with Home Ownership Would Be... Understanding the Hidden Costs

Owning a home is a significant life goal, but understanding the full financial picture is crucial. While the purchase price is a substantial outlay, the ongoing expenses associated with home ownership often create a larger financial burden than many anticipate. This article delves into the major recurring expenses that frequently accompany home ownership, helping you prepare for the long-term commitment.

- Unveiling the Mortgage Maze

- Beyond the Mortgage: Additional Financial Obligations

- Property Taxes and Insurance: Essential Protections

- Maintaining Your Investment: Ongoing Costs

- HOA Fees and Utility Costs: Understanding Additional Expenses

-

Key Takeaways

- Frequently Asked Questions about Major Homeownership Expenses

- What are the biggest ongoing expenses after buying a home?

- How do mortgage payments work, and how are they affected?

- What is Private Mortgage Insurance (PMI), and when is it required?

- How are property taxes calculated, and what are the tax consequences of not paying them?

- How important is homeowners insurance, and what does it cover?

- What about maintenance and repairs, and how much should I budget each year?

- Are there additional costs associated with owning a home?

Unveiling the Mortgage Maze

The mortgage itself is arguably the largest recurring expense. The principal and interest payments, dependent on the interest rate and loan terms, form the core of your monthly budget. Choosing between 30-year fixed-rate mortgages and adjustable-rate mortgages (ARMs) significantly impacts your financial commitment. A 30-year fixed mortgage, while offering lower monthly payments, results in a higher total interest paid over the life of the loan. Conversely, ARMs offer lower initial payments but have fluctuating interest rates, creating financial uncertainty. Understanding the implications of different loan structures is crucial in budgeting for your mortgage. Borrowers should carefully consider the potential impacts of interest rate fluctuations before choosing an ARM.

Beyond the Mortgage: Additional Financial Obligations

Comprehending the full spectrum of homeownership expenses requires looking beyond the mortgage payment. A significant factor is the Private Mortgage Insurance (PMI), often required if your down payment is less than 20% of the home's value. This insurance adds an additional cost of 0.5-2% annually to your mortgage payments. Government-backed loans, such as FHA loans, frequently mandate PMI for the duration of the loan. Understanding these additional costs is essential in creating a realistic budget.

Property Taxes and Insurance: Essential Protections

Property taxes are another major expense, often determined by the assessed value of your home. Property values tend to increase over time, which often leads to increasing tax bills as well. Failure to pay property taxes can result in significant consequences, including liens, potential foreclosure, or even the sale of your property to investors. Equally crucial is homeowners insurance, which safeguards against potential financial losses from damages. Different policies have various coverage details, including dwelling coverage, personal property coverage, and liability coverage. Essential additional coverage includes disaster coverage, protecting against flood, earthquake, or other natural disasters, which can significantly increase insurance premiums.

Maintaining Your Investment: Ongoing Costs

Home maintenance and repairs represent a critical component of the overall homeownership cost. Budgeting 1-3% of your home's value annually for maintenance and repairs is crucial, considering potential structural repairs like foundation issues, roof replacements, or window upgrades. You should also include planned maintenance for mechanical systems such as furnaces, water heaters, and HVAC systems in your annual budget.

HOA Fees and Utility Costs: Understanding Additional Expenses

Association fees are a significant consideration for condominium or townhouse owners, or those in planned communities. These fees typically cover maintenance and upkeep of shared facilities and areas, but can also include special assessments for unforeseen major repairs. Understanding the financial status of your HOA is crucial to mitigate potential financial surprises. Utilities, including electricity, water, gas, internet, and any additional local costs, are recurring expenses that will vary seasonally influenced by climate. A thorough understanding of utility costs in your area is essential when creating a comprehensive home ownership budget.

Key Takeaways

Preparing for homeownership involves meticulous financial planning that extends beyond the initial purchase price. Understanding the long-term implications of different mortgage types, PMI, property taxes, insurance, maintenance costs, HOA fees, and utility expenses is crucial to avoid financial surprises and achieve a sustainable budgeting strategy. Creating a comprehensive financial plan that accounts for all these expenses is critical to ensuring financial success in homeownership.

Frequently Asked Questions about Major Homeownership Expenses

This FAQ section addresses key financial considerations associated with owning a home beyond the initial purchase price.

What are the biggest ongoing expenses after buying a home?

The largest ongoing expenses after purchasing a home are typically mortgage payments, property taxes, homeowners insurance, and maintenance/repairs. These costs can significantly impact a homeowner's budget and require careful planning and budgeting. Other recurring costs, such as utility bills and potential HOA fees, also need to be considered.

How do mortgage payments work, and how are they affected?

Mortgage payments consist of principal and interest. The amount you pay each month depends on the interest rate, loan term (e.g., 15-year vs. 30-year), and the loan amount itself. Interest rates fluctuate, so adjustable-rate mortgages (ARMs) can bring added financial uncertainty while fixed-rate mortgages offer stability. Loan terms directly affect the total interest paid over the life of the loan.

What is Private Mortgage Insurance (PMI), and when is it required?

Private Mortgage Insurance (PMI) is a type of insurance required if you put less than 20% down on a home. It protects the lender in case you default on the loan. The annual premiums for PMI typically range from 0.5% to 2% of the loan amount. Government-backed loans, like FHA loans, often require PMI for the entire loan term, regardless of the down payment.

How are property taxes calculated, and what are the tax consequences of not paying them?

Property taxes are calculated based on the assessed value of your home. Each jurisdiction has its own tax rate, which can vary significantly. Failure to pay property taxes can result in serious consequences, including liens on your property, potential foreclosure, or even the sale of your home to investors.

How important is homeowners insurance, and what does it cover?

Homeowners insurance is essential to protect against financial losses from damage to your home, its contents, and potential liability claims arising from incidents on your property. Standard policies typically cover the dwelling itself, personal belongings, and liability in case of accidents. Specific coverage for disasters, such as floods, earthquakes, or hail, is crucial but often comes with higher premiums. Factors like home value, location, construction materials, and your credit history impact premium rates.

What about maintenance and repairs, and how much should I budget each year?

Regular maintenance is vital to prevent costly repairs later. Budgeting 1-3% of your home's value annually for maintenance and repairs is a general guideline. This covers everything from minor upkeep to replacing essential systems and components, like roofs, windows, and heating/cooling systems. HOA fees, if applicable, must also be taken into account.

Are there additional costs associated with owning a home?

Beyond the core expenses, several additional costs can arise. These include utility bills (electricity, gas, water, internet), potential HOA fees, and special assessments for major repairs, which may be required by homeowner's associations or other governing bodies. Seasonal variations in weather can also affect utility bills, impacting your overall budgeting.