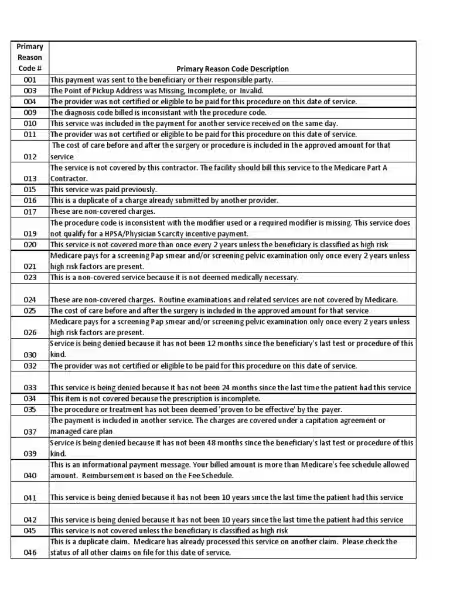

PR 21 Denial Code: Navigating No-Fault Claims in Healthcare

Understanding and successfully addressing denial code PR 21 is crucial for healthcare providers and patients alike. This code signifies that an insurance company has rejected a claim, not due to procedural errors or lack of coverage, but because it believes a different insurer (typically auto or workers' compensation) has primary responsibility. This article will delve into the intricacies of PR 21 denial code, exploring its implications and providing actionable strategies for resolution.

- Deciphering the PR 21 Denial Code

- Unraveling the Reasons Behind PR 21

- Strategies for Addressing PR 21 Denials

-

Prevention and Proactive Measures

- Proactive Strategies

- What is Denial Code 21?

- What is "No-Fault" Insurance?

- Why Does Denial Code 21 Occur?

- How Can Healthcare Providers Address a Denial Code 21?

- How Can Patients Help Prevent Denial Code 21?

- What Should Be Included in Patient Medical Records?

- What if the No-Fault Insurer Denies the Claim?

Deciphering the PR 21 Denial Code

Denial Code 21, often referred to as PR 21, signifies a crucial shift in responsibility for payment. It's not a reflection on the quality of the healthcare provided, but rather a determination that an alternative insurance entity, usually involved with no-fault accidents or workplace injuries, is obligated to cover the costs. This distinction is pivotal because it directly impacts the avenues available for a successful claim resolution. The initial insurer, the one receiving the claim, is refusing payment not because of any flaw in the claim, but due to the perceived liability of a third-party carrier.

The underlying principle is no-fault insurance systems. These systems determine coverage based on the accident's nature, not fault. For example, if the patient's injury stems from a car accident, the auto no-fault insurer is usually the primary payer. This paradigm aims to expedite compensation and prevent disputes over liability. However, successfully navigating these claims requires a deep understanding of the specific circumstances.

Unraveling the Reasons Behind PR 21

A critical aspect of understanding PR 21 is recognizing the nuances behind these denials. Simply stated, the rejection arises from a belief that another entity, typically involved in no-fault insurance, should be the primary payer. This belief hinges on concrete evidence tying the injury to a specific event such as a car accident or workplace incident. This often means the insurance company initially processing the claim needs to verify that the injury falls under the purview of the appropriate no-fault or workers' compensation coverage.

Determining the specific cause of the injury is crucial. Was it a workplace injury? A result of a verifiable car accident? The nuances of the accident or event are critical elements. The insurance company assessing the PR 21 denial needs to understand if a no-fault carrier's coverage applies. This is often dependent on the specifics of the incident, local regulations, and the applicable no-fault insurance laws.

Strategies for Addressing PR 21 Denials

Navigating PR 21 denials requires a multi-pronged approach. For healthcare providers, meticulous documentation is paramount. This includes comprehensive records of the incident, patient accounts, police reports (if available), and any other corroborating evidence.

Crucial Documentation for Providers

- Precise details of the incident: Exact time, location, and circumstances.

- Patient statements (where permitted): Account of the events leading to injury.

- Supporting documentation: Police reports, witness statements, accident reports.

- Medical records: Thorough documentation of the injury, treatment, and procedures performed.

For both healthcare providers and patients, understanding the specific nuances of no-fault insurance laws in the relevant jurisdiction is vital. These laws often dictate specific procedures and timelines for reporting and handling such claims.

Key Steps for Resolution

- Thorough review of the denial notice: Identify the specific reason for the denial and the designated no-fault carrier.

- Gathering crucial information: Collect patient information, medical records, no-fault insurance details, and accident specifics.

- Communication with the patient: Obtain complete details of the accident from the patient.

- Coordination of benefits (COB): Coordinate benefits with all relevant carriers, proving exhaustion of no-fault coverage.

- Filing with the no-fault carrier: File the claim with the appropriate no-fault carrier, adhering to their specific guidelines and timelines.

- Formal appeal to the primary health insurer: If the claim is denied by the no-fault carrier, formally appeal to the primary health insurer, providing all supporting documentation.

Prevention and Proactive Measures

Proactive measures can prevent PR 21 denials. Healthcare providers should train staff to gather relevant information about no-fault insurance during patient registration. This upfront information gathering can significantly reduce the incidence of these denials. Educating billing teams about procedures and prevention strategies is equally important.

Proactive Strategies

- Comprehensive patient intake forms: Gather no-fault insurance details during patient registration.

- Training for staff: Educate staff on gathering accident details and relevant documentation.

- Clear communication protocols: Establish clear communication channels and processes for handling no-fault claims.

- Regular review of no-fault regulations: Stay updated on changes in no-fault laws and regulations.

Ultimately, understanding PR 21 denial codes and the complexities of no-fault insurance is crucial for efficient claim processing and successful patient outcomes. A comprehensive approach, incorporating meticulous documentation, clear communication, and proactive measures, can effectively mitigate the challenges. Consulting with legal counsel or insurance professionals can significantly assist in navigating these complex disputes.

What is Denial Code 21?

Denial Code 21, in the context of healthcare claims, signifies that the insurance company processing the claim is refusing payment because it believes a different insurer (typically auto or workers' compensation) is responsible for the patient's injury or illness. This denial isn't due to procedural errors or quality issues with the claim itself, but rather a perceived shift in responsibility to another insurer. It's often associated with "no-fault" insurance systems.

What is "No-Fault" Insurance?

"No-fault" insurance systems, prevalent in some states, cover medical expenses related to an accident or injury without determining fault or liability. This means the primary insurer may deny payment if they believe the responsible party's insurer (e.g., auto or workers' comp) should be covering the claim.

Why Does Denial Code 21 Occur?

Denial Code 21 can occur for several reasons, including:

- Auto Accidents: Claims related to car accidents are often the responsibility of the no-fault insurer.

- Work-Related Injuries: Injuries sustained at work may be covered by workers' compensation insurance.

- Incomplete or Incorrect Documentation: Lack of evidence of the incident, patient statements, or police reports can lead to denial.

- Failure to Identify the Correct Insurer: The healthcare provider may not have the correct information about the no-fault policy or the responsible insurer.

- Missing Coordination of Benefits (COB) Information: Information about other insurance policies the patient may have is crucial for proper claim handling.

How Can Healthcare Providers Address a Denial Code 21?

- Thorough Review of the Denial Notice: Identify the specific reason for denial and the correct no-fault insurer.

- Gather Complete Documentation: Collect all relevant information, including patient statements, police reports, witness statements, accident details, and the no-fault policy information.

- Contact the Patient for Details: Obtain precise details about the incident from the patient.

- Identify and Contact the No-Fault Insurer: File the claim with the appropriate no-fault insurer, following their specific guidelines.

- Coordinate Benefits: Ensure proper coordination of benefits with all relevant insurers to avoid double payments or coverage gaps.

- Appeal the Denial: If the no-fault insurer denies the claim, appeal the original denial to the primary health insurer, providing all supporting documentation.

- Seek Legal or Insurance Advice: Due to complexities in no-fault claims, consulting a legal professional or insurance expert is recommended to understand the best course of action.

How Can Patients Help Prevent Denial Code 21?

- Provide Accurate Information: Patients should provide accurate and detailed information about the accident or incident, including their no-fault insurance details.

- Communicate with Their Insurers: Patients should keep their healthcare providers updated on any relevant insurance information or changes.

What Should Be Included in Patient Medical Records?

Medical records should include detailed information about the incident, including:

- Precise details of the accident or incident: Time, location, circumstances, and any witnesses.

- Patient statements: If legally permissible, accurate accounts of the incident from the patient.

- Supporting documentation: Police reports, witness statements, and any other relevant evidence.

What if the No-Fault Insurer Denies the Claim?

If the no-fault insurer denies the claim, a formal appeal to the primary health insurer is necessary, providing all supporting documentation.